What is a Credit Score?

A credit score is a three-digit number (typically between 300 and 900) that represents your creditworthiness — essentially, how reliable you are when it comes to borrowing and repaying money.

In India, this score is generated by credit bureaus such as TransUnion CIBIL, based on your financial behavior. The higher your score, the more trustworthy you appear to lenders like banks and NBFCs.

A good credit score indicates:

- Timely repayment of loans and credit card bills

- Responsible credit usage

- Low risk of default

A poor score, on the other hand, signals potential risk, making lenders hesitant to approve your loan or offer favorable terms.

How CIBIL Works

TransUnion CIBIL is India’s most widely used credit bureau. It collects and maintains records of your credit activity from banks and financial institutions.

How the system works:

Data Collection

Banks and lenders report your credit behavior (loan repayments, credit card usage, defaults, etc.) to CIBIL regularly.

Credit Report Generation

This data is compiled into a Credit Information Report (CIR).

Score Calculation

Based on your CIR, a credit score (300–900) is calculated using proprietary algorithms.

Lender Access

When you apply for a loan or credit card, lenders check your CIBIL report and score to assess risk.

You don’t “apply” for a score — it is automatically generated based on your financial activity.

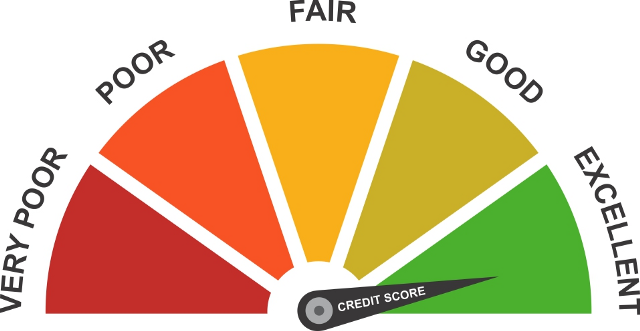

Credit Score Ranges (300–900)

Factors Affecting Your Credit Score

Your credit score is influenced by multiple factors. Understanding them helps you improve and maintain a healthy score.

Payment History (Most Important)

- Late payments, missed EMIs, or defaults significantly lower your score

- Consistent on-time payments boost it

Credit Utilization Ratio

- This is the percentage of your credit limit you use

- Ideally, keep it below 30%

- High usage signals credit dependency

Credit Mix

A healthy mix of secured loans (home/car) and unsecured loans (credit cards/personal loans) improves your profile

Length of Credit History

- Longer credit history = more reliability

- Closing old accounts can sometimes reduce your score

Hard Inquiries

- Every time you apply for credit, lenders check your report

- Too many applications in a short period can lower your score

Outstanding Debt

High unpaid balances negatively impact your score

How Credit Score Impacts Loans

Your credit score directly affects your financial opportunities:

Loan Approval

- High score → Easier and faster approvals

- Low score → Higher chances of rejection

Interest Rates

- Higher score → Lower interest rates

- Lower score → Higher interest rates (risk premium)

Loan Amount

- Good score → Higher loan eligibility

- Poor score → Limited borrowing capacity

Credit Card Benefits

- Premium cards and higher limits are offered to individuals with strong scores

Negotiation Power

With a high score, you can negotiate better loan terms and fees

Conclusion

In the modern financial ecosystem of India, a credit score has evolved into a critical benchmark that defines an individual’s financial credibility and access to credit. It is no longer just a number used during loan applications, but a comprehensive reflection of one’s financial discipline, repayment behavior, and overall credit management. Lenders, particularly institutions that rely on data from TransUnion CIBIL, use this score as a primary tool to evaluate risk, determine eligibility, and structure loan terms.

A consistently strong credit score not only improves the likelihood of loan approvals but also places borrowers in a position of advantage, enabling them to secure lower interest rates, higher credit limits, and more flexible repayment options. Conversely, a weak score can restrict financial opportunities, increase borrowing costs, and signal instability to potential lenders. This makes it essential for individuals to view their credit score as a long-term financial asset rather than a short-term requirement.

Maintaining a healthy credit profile requires sustained financial discipline, including timely repayments, prudent credit utilization, and careful management of borrowing habits. Over time, these practices contribute to building a trustworthy financial identity that can support major life goals such as purchasing a home, financing education, or expanding a business.

Ultimately, understanding how credit scoring systems work and proactively managing one’s credit behavior empowers individuals to take control of their financial future. In an increasingly credit-driven economy, a strong credit score serves not just as an eligibility metric, but as a gateway to better financial opportunities and long-term stability.